Accounts - Class 11

-

CHAP 1 - FUNDAMENTALS OF BOOK KEEPING AND ACCOUNTANCY

Videos - Introduction to Accountancy7 Topics -

Introduction to Accounting

-

Account and its Classification8 Topics

-

হিসাবখাত কি? (What is an Account?)

-

হিসাবখাতের শ্রেণীবিভাগ (Classification of Accounts)

-

ব্যক্তিক হিসাবখাত, সম্পত্তি-সঙ্ক্রান্ত হিসাবখাত ও নামিক হিসাবখাতের মধ্যে তুলনামূলক আলোচনা (Distinguish between and benefits of types of accounts)

-

Selection of atleast two Accounts

-

Some examples of Choice of Accounts

-

Why should we ignore the answer - "Goods"

-

Expenses incurred vs. Asset Bought

-

Examples of Accounts and their Classification

-

হিসাবখাত কি? (What is an Account?)

-

Event and Transaction7 Topics

-

ভূমিকা (Introduction to Events and Transactions)

-

ঘটনা (Event)

-

লেনদেন (Transaction)

-

লেনদেনের বৈশিষ্ট্য (Salient features of transaction):

-

লেনদেনের প্রকারভেদ (Classification of transaction)

-

ঘটনা এবং লেনদেনের মধ্যে পার্থক্য (Difference between event and transaction)

-

ঘটনা কে লেনদেন হিসেবে স্বীকৃতি দেওয়ার জন্য বিবেচ্য বিষয় সমূহ (Recognising an event as a transaction)

-

ভূমিকা (Introduction to Events and Transactions)

-

Fundamental Accounting Terms37 Topics

-

পণ্য সামগ্রী (Goods)

-

সম্ভার / মজুত সামগ্রী / মজুতপণ্য (Stock-in-trade / Inventory)

-

ক্রয়/ খরিদ (Purchases)

-

আমদানি (Import)

-

ক্রয় ফেরত (Purchase Return/Return Outward)

-

বিক্রয় (Sales)

-

রপ্তানি (Export)

-

বিক্রয় ফেরত (Sales Return / Return Inward)

-

প্রদান (Payments)

-

ব্যয় (Expenditure)

-

খরচ (Expenses)

-

ব্যয় ও খরচের মধ্যে পার্থক্য (Difference between Expenditure and Expenses)

-

ক্ষতি / লোকসান (Losses)

-

মাশুল (Freight)

-

পণ্য সংক্রান্ত বহন খরচ (Carriage)

-

বাট্টা (Discount)

-

ব্যবসায়িক বাট্টা ও নগদ বাট্টার পার্থক্য (Difference between Trade Discount and Cash Discount)

-

অফিসে ব্যবহৃত সামগ্রী (Office Stationery)

-

প্রাপ্তি (Receipts)

-

মোট আয় (Revenue)

-

আয় (Income)

-

মুনাফা (Profit)

-

লাভ/ফায়দা (Gains)

-

পরিব্যয় (Cost)

-

দায় (Liabilities)

-

মূল্ধন (Capital)

-

উত্তোলন (Drawings)

-

মালিক / উদ্যোক্তা / ব্যবসায়ী (Proprietor / Entrepreneur / Businessman)

-

বানিজ্যিক প্রদেয় (Trade Payable)

-

পাওনাদার (Creditors)

-

প্রদেয় হুন্ডি (Bills payments)

-

সম্পত্তি (Assets)

-

দেনাদার (Debtors)

-

প্রাপ্য হুন্ডি (Bills Receivable)

-

বিনিয়োগ (Investments)

-

হিসাবশস্ত্রে ব্যবহৃত আরও কিছু অন্যান্য গুরুত্বপূর্ণ শব্দাবলী (Miscellaneous Terms)

-

Recap Session on Event, Transaction and Important Business Terms

-

পণ্য সামগ্রী (Goods)

-

Chapter Exercise1 Quiz

-

Chap 2 - JournalVideos - Journal12 Topics

-

Journal

-

Journal Sum 1

-

Journal Sum 2

-

Initial Concept on GST

-

Items on which GST payable

-

Items on which GST is receivable

-

Items on which reversal of GST is levied

-

Cascading Effect of GST

-

Practical Sums Relating to GST

-

Areas on which GST is not levied

-

Journal Entries on Special Area Transactions

-

Module Revision - Journal

-

Journal

-

Double Entry Principle10 Topics

-

দ্বিতরফা দাখিলা পদ্ধতির ভিত্তি

-

Debit and Credit

-

দ্বিতরফা দাখিলা পদ্ধতির বৈশিষ্ট্য (Features of Double Entry System)

-

দ্বিতরফা দাখিলা পদ্ধতির সুবিধা (Advantages of Double Entry System)

-

তরফা দাখিলা পদ্ধতির অসুবিধা (Disadvantages of Double Entry System)

-

সুবর্ণ নিয়মাবলী (Golden rule of accounting)

-

আমেরিকান সমীকরণ পদ্ধতি (American Equation)

-

Eventualities of American Equation Approach

-

Analysing the Transactions with Both the Rules

-

Ascertainment of Debit and Credit

-

দ্বিতরফা দাখিলা পদ্ধতির ভিত্তি

-

Special Area Transactions2 Topics

-

Chapter Excercise2 Topics|1 Quiz

-

Practical Sums - Journal2 Topics

-

Chap 3 - Ledgerএই অধ্যায়টি পাঠের উদ্দেশ্য (Why should students learn this chapter?)

-

Videos - Ledger14 Topics

-

Introduction to Ledger

-

Basic Transaction and Ledger Posting

-

Purchase related transactions and Ledger posting

-

Sales related transactions and Ledger posting

-

Income and Expense related transactions and Ledger posting

-

Posting of Bank and Cheque related transactions

-

Posting and Balancing of Adjustment Entries

-

Debtors Ledger and Creditors Ledger

-

Calculation of Missing figures Part 1

-

Calculation of Missing figures Part 2

-

Calculation of Missing figures Part 3

-

Ledger posting and GST of Purchase Related Transaction

-

Ledger posting and GST of Sales Related Transaction

-

Ledger Recap Session and importance of certain terms

-

Introduction to Ledger

-

Ledger Introduction theory3 Topics

-

খতিয়ানের উপবিভাগ (Sub-division of Ledger)2 Topics

-

Ledger Format and Posting3 Topics

-

Relation between Journal and Ledger4 Topics

-

Balancing a Ledger5 Topics

-

হিসেবের জের টানা (Balancing Mechanism of a Ledger Account)

-

একটি চিত্রের মারফত হিসেবখাতের জের টানার পদ্ধতিটি ব্যাখ্যা করা হলঃ (How to make a ledger account)

-

প্রারম্ভিক জের ও অন্তিম জেরের জন্য ব্যবহৃত পরিভাষা গুলির অর্থ (Concept of Initial and Final Balance)

-

হিসেবখাতের জের টানার প্রয়োজনীয়তা (Need for Balancing of a Ledger Account)

-

এবার এক নজরে দেখে নেওয়া যাক হিসাবখাতের প্রকৃতি অনুযায়ী কোন হিসাবখাতের প্রারম্ভিক জের কি হতে পারে?

-

হিসেবের জের টানা (Balancing Mechanism of a Ledger Account)

-

Module 13 - A Complete Sum on Ledger posting and Balancing

-

Chapter Revision - Ledger

-

Chapter Exercise2 Topics|1 Quiz

-

Chap 4 - Books of Original EntriesIntroduction to Books of Original Entries1 Topic

-

Videos - Cash Book9 Topics

-

Introduction to Books of Original Entry

-

Introduction to Cash Book and Format

-

Sum on Single Column Cash Book

-

Sum 1 on Double Column Cash Book and Balancing

-

Sum 2 on Double Column Cash Book and Balancing

-

Sum 3 on Double Column Cash Book and Balancing

-

Double Column Cash Book with Discount and GST concept

-

Triple Column Cash Book and Balancing

-

Triple Column Cash Book with Discount and GST concept

-

Introduction to Books of Original Entry

-

Special Purpose Books I-Cash Book11 Topics

-

ভুমিকা

-

নগদান বই বলতে কি বোঝো? (What Cash Book is?)

-

নগদান বইয়ের বৈশিষ্ট্য (Features of Cash Book)

-

নগদান বইয়ের সুবিধা বা উপযোগিতা (Advantages or Utility of Cash Book)

-

নগদান বই প্রস্তুত করণের জন্য প্রয়োজনীয় উৎসনথি (Source Documents which will help to prepare Cash Book properly)

-

নগদান বই জাবেদা না খতিয়ান? (Is cash book a Journal or a Ledger?)

-

নগদান বই ও জাবেদার মধ্যে পার্থক্য (Difference between Cash Book and Journal)

-

নগদাণ বই ও খতিয়ানের মধ্যে পার্থক্য (Difference between Cash Book and Ledger)

-

নগদান বই ও নগদান হিসাবখাতের মধ্যে পার্থক্য (Difference between Cash Book and Cash Account)

-

নগদান বইয়ের শ্রেনীবিভাগ (Clssification of Cash Book)

-

Chapter Revision - Cash Book

-

ভুমিকা

-

Videos - Petty Cash Book6 Topics

-

Special Purpose Books I- Petty Cash Book10 Topics

-

ভূমিকা (Introduction)

-

খুচরো নগদান বই বলতে কি বোঝ? (What is Petty Cash Book?)

-

খুচরো নগদান বইয়ের বৈশিষ্ট্য (Features of cash Book)

-

খুচরো নগদান বইয়ের উপযোগিতা (Advantages or Need for maintaining Petty Cash Book)

-

খুচরো নগদান বই প্রস্তুতকরণ বিভিন্ন পদ্ধতি (Various methods for preparing Petty Expenses in a Petty Cash Book)

-

বিভিন্ন প্রকার খুচরো নগদান বইয়ে লেনদেন গুলি লিপিবদ্ধ করণের জন্য অনুসৃত নিয়ম সমূহ (Rules of recording transactions in a petty Cash Book

-

একনজরে কিছু সমজাতীয় খুচরো খরচ এবং সেই খরচের সঙ্গে সংশ্লিষ্ট নির্দিষ্ট খরচ হিসাবখাত গুলি ব্যাখ্যা সহ আলোচনা করা হল (Main heads of Petty Expenses Accounts under which various petty expenses are taken)

-

খুচরো নগদান বই থেকে খতিয়ানে হিসাব তোলা (Ledger Posting from petty Cash Book)

-

সরল পদ্ধটি এবং বৈশ্লেষিক পদ্ধটিতে রক্ষিত খুচরো নগদান বইয়ের মধ্যে পার্থক্য (Differences between Simple Petty Cash Book and Analytical Petty Cash Book)

-

Chapter Revision - Petty Cash Book

-

ভূমিকা (Introduction)

-

Videos - Other Day Books14 Topics

-

Introduction to Purchase Day Book and Sum on Simple type Purchase Book

-

Single Column Purchase Day Book with Sum

-

Sum on Multi Column Purchase Day Book

-

Multi Column Purchase Day Book with GST and Balancing

-

Simple type Sales Day Book without GST

-

Simple type Sales Day Book with more than one product

-

Sales Day Book with GST

-

Purchase Return Book with and without GST

-

Sales Return Book with and without GST

-

Recap Session on Day Books

-

Journal Proper - Opening Entry

-

Journal Proper - Closing Entry and Transfer Entry

-

Journal Proper - Adjustment Entries

-

Journal Proper - Credit Purchase and Sale of Asset and Residuary Entries

-

Introduction to Purchase Day Book and Sum on Simple type Purchase Book

-

Special Purpose Books II -Other Books7 Topics

-

Practical Sums - Books of Original Entries4 Topics

-

Chapter Excercise6 Topics|3 Quizzes

-

অতি সংক্ষিপ্ত প্রশ্ন উত্তর (SHORT ANSWER TYPE QUESTIONS) - Cash Book

-

রচনাধর্মী প্রশ্ন (LONG ANSWER TYPE QUESTIONS) - Cash Book

-

অতি সংক্ষিপ্ত প্রশ্ন উত্তর (SHORT ANSWER TYPE QUESTIONS) - Petty Cash Book

-

রচনাধর্মী প্রশ্ন (LONG ANSWER TYPE QUESTIONS) - Petty Cash Book

-

অতি সংক্ষিপ্ত প্রশ্ন উত্তর (SHORT ANSWER TYPE QUESTIONS) - Other Book

-

রচনাধর্মী প্রশ্ন (LONG ANSWER TYPE QUESTIONS) - Other Book

-

অতি সংক্ষিপ্ত প্রশ্ন উত্তর (SHORT ANSWER TYPE QUESTIONS) - Cash Book

-

Chap 5 - Rectification of ErrorsVideos - Rectification of Errors14 Topics

-

Concept of Rectification of Error

-

List of Errors

-

Stages of Error Detection and Single Sided Errors

-

Double Sided Errors

-

Analysis of Error of Commission

-

Analysis of Error of Commission 2

-

Analysis of Error of Commission and Compensating Error

-

Analysis of Error of Principle

-

Analysis of Capital Expenditure treated as Revenue Expenditure

-

Example 1

-

Example 2

-

Example 3

-

Example 4

-

Recap Session on Rectification of Errors

-

Concept of Rectification of Error

-

ভূমিকা

-

হিসাবশাস্ত্রের ভুল এবং তার প্রকারভেদ (Different types of Error in Accounting & classification of Errors)

-

কিছু হিসাব সংক্রান্ত ভুলত্রুটি যা রেওয়ামিল প্রস্তুতকালে নির্ধারণ করা সম্ভব (Types of Errors that can be detected while preparing Trial Balance)

-

কিছু হিসাব সংক্রান্ত ভুলত্রুটি যা রেওয়ামিল প্রস্তুতকালে নির্ধারণ করা সম্ভব নয় (Types of Errors that cannot be detected while preparing Trial Balance)

-

ভুলসংশোধন দাখিলা বনাম মিলকরণ দাখিলা (Rectification Entry v/s Adjustment Entry)

-

হিসাবনিকাশকরনের ক্ষেত্রে একতরফা, দ্বিতরফা ভুল এবং মিশ্র ভুল বলতে কি বোঝানো হয়? (What is Single-sided or One-sided error, Double-sided error and Mixed error in Accounting?)

-

ভুল উদ্ঘাটন এবং সংশোধনের বিভিন্ন পর্যায় (Various stages of detection and rectification of errors)

-

অনিশ্চিত হিসাবখাত (The Suspense Account)

-

হিসাব বইয়ের ভুল ধরার পদ্ধতি

-

কিছু সাহায্যকারী বই সংক্রান্ত ভুল এবং তার সংশোধন পদ্ধতি (Errors in Subsidiary Books and procedure for rectification)

-

এমন কিছু হিসাব সংক্রান্ত ভুল যার দ্বারা একাধিক হিসাবখাত প্রভাবিত অথচ অনিশ্চিত হিসাব বা Suspense A/c-এর উদ্ভব ঘটেনি (Errors Which Affect Multi Accounts Simultaneously Without the Appearance of Suspense Account)

-

পূর্ণাঙ্গ বিষয়মুখী ব্যবহারিক সমস্যা (A comprehensive problem)

-

Chapter Revision - Rectification of Errors

-

Practical Sums - Rectification of Errors4 Topics

-

Chapter Exercise2 Topics|1 Quiz

-

Chap 6 - Bank Reconciliation StatementVideos - Bank Reconciliation Statement10 Topics

-

Introduction to BRS

-

Explanation of BRS with an example

-

Causes of disagreement between Cash Book balance and Pass Book balance

-

Comprehensive Sum on BRS

-

Sum on BRS with two bank accounts

-

Concept of Overdraft and BRS with Overdraft balance as per Cash Book and Pass Book

-

BRS with Overdraft balance as per and Pass Book

-

BRS with Amended Cash Book

-

Concept of Overdraft

-

Recap Session on BRS

-

Introduction to BRS

-

ভূমিকা

-

আমানতকারী প্রতিষ্ঠান বা কারবারীর সঙ্গে তার ব্যাংকস্থিত চলতি আমানতের সম্পর্ক (Relation between the trader and his concerned bank Current Account)

-

ব্যাংক পাস বই ও ব্যাংক বিবরণী (Bank Pass Book and Bank Statement)

-

ব্যাংক সমন্বয় বিবৃতি কি? (What is Bank Reconciliation Statement?)

-

নগদান বই এবং পাস বইয়ের মধ্যে পার্থক্য (Difference between Cash Book and Pass Book)

-

নগদান বই ও পাস বইয়ের জেরের গরমিলের কারণ (Causes of disagreement between Bank Balance as per Cash Book and Pass Book)

-

একনজরে নগদান বই সংক্রান্ত এবং পাস বই সংক্রান্ত যে যে কারণ গুলির জন্য হস্তস্থ নগদান বইয়ের ব্যাংকস্থিত জের এবং ব্যাংক মারফৎ রক্ষিত আমানতকারী কারবারি সংক্রান্ত হিসাবখাতটির জেরের মধ্যে অসঙ্গতি লক্ষ্য করা যায় (Reasons for which Cash Book balance differs from Pass Book at a glance)

-

ব্যাংক হিসাব মিলকরণ বিবরণীর বৈশিষ্ট্য (Features of Bank Reconciliation Statement)

-

ব্যাংক হিসাবমিলকরণের সুবিধা / প্রয়োজনীয়তা / উপযোগিতা (Advantages or Necessities / Utilities of Bank Reconciliation Statement)

-

কেনো একটি নির্দিষ্ট দিনে কেন নগদান বইয়ের জের পাস বই অপেক্ষা ভিন্ন হয়? (Why should Cash Book Balance differ from Pass Book Balance on a particular date?)

-

ব্যাংক সমন্বয় বিবৃতি একটি নির্দিষ্ট দিনে বিশেষত আর্থিক হিসাবকালের শেষ দিনে কেন প্রস্তুত করা হয়? (Why is Bank Reconciliation Statement prepared as on a particular date mainly the closing date of accounting year?)

-

ব্যাংক মিলকরণ বিবৃতি কি একটি হিসাবখাত? (Is Bank Reconciliation Statement an Account?)

-

ব্যাংক সমন্বয় বিবৃতি প্রস্তুতকরণ পদ্ধতি (How to prepare Bank Reconciliation Statement)

-

প্রথম পদ্ধতি ব্যাংক সমন্বয় বিবৃতির ছক (Proforma of a Bank Reconciliation Statement under First Method)

-

দ্বিতীয় বিকল্প

-

দ্বিতীয় পদ্ধতি ব্যাংক সমন্বয় বিবৃতির ছক (Proforma of a Bank Reconciliation Statement under Second Method)

-

ব্যাংক সমন্বয় বিবৃতির প্রকৃত পরীক্ষা (The true test of Bank Reconciliation Statement)

-

কিছু কার্যকরী টিপ্পনী যা শুদ্ধভাবে একটি ব্যাংক সমন্বয় বিবৃতি প্রস্তুত করতে বিশেষভাবে সহায়ক (Few tips to make an appropriate Bank Reconciliation Statement)

-

ব্যাংক জমাতিরিক্ত এবং ব্যাংক সমন্বয় বিবৃতির ওপর তার প্রভাব (Bank Overdraft and its implementation in Bank Reconciliation Statement)

-

সংশ্লিষ্ট Cash Book বা Pass Book-এর গণনা সংক্রান্ত ভুল (Casting Errors in Cash Book or Pass Book)

-

Chapter Revision - Bank Reconciliation Statement

-

Practical sums Bank Reconciliation Statement5 Topics

-

Chapter Exercise2 Topics|1 Quiz

-

Chap 7 - Trial BalanceVideos - Trial Balance7 Topics

-

ভূমিকা

-

রেওয়ামিল বলতে কি বোঝায়? (What is Trial Balance?)

-

রেওয়ামিলের ছক (Specimen/proforma of a Trial Balance)

-

বিবিধ হিসাবখাত এবং রেওয়ামিলে অন্তর্গত তাদের জের (Various accounts and their balances in trial balance with reasons)

-

GST সংক্রান্ত খতিয়ান এবং তাদের জের (GST related ledger account balances along with the reasons)

-

অন্তিম মজুত পণ্য এবং তার অবস্থান (Position of closing stock in Trial Balance)

-

রেওয়ামিল প্রস্তুতকরণ পদ্ধতি (Steps for preparing Trial Balance)

-

রেওয়ামিলের বৈশিষ্ট্য (Features/ characteristics of Trial Balance)

-

রেওয়ামিলের ডেবিট দিক এবং ক্রেডিট দিক না মিললে যে যে ধাপ অনুসৃত হয় (Steps which are taken where Trial Balance does not agree, i.e., total of debit side is no equal to total of credit side)

-

অনিশ্চিত হিসাবখাত – উদ্ভব এবং বিলুপ্তি (The Suspense Account in Trial Balance ---- Occurrence and its Abolishment)

-

GST বহির্ভূত একটি রেওয়ামিল যেখানে সংশ্লিষ্ট লেনদেন গুলিকে জাবেদায়িত করণের পর সেগুলিকে ক্ষতিয়ানে অন্তর্ভুক্ত করে অতঃপর রেওয়ামিল প্রস্তুত করা হয়েছে

-

যখন সংশ্লিষ্ট হিসাবখাত গুলির জের গুলি প্রদত্ত – এমত অবস্থায় রেওয়ামিল প্রস্তুত করণ

-

GST সহ একটি রেওয়ামিল যেখানে সংশ্লিষ্ট লেনদেন গুলিকে জাবেদায়িত করণের পর সেগুলিকে ক্ষতিয়ানে অন্তর্ভুক্ত করে অতঃপর রেওয়ামিল প্রস্তুত করা হয়েছে

-

অশুদ্ধ রেওয়ামিল শুদ্ধ করার পদ্ধতি (How to Rectify an incorrect Trial Balance)

-

রেওয়ামিলের কার্যাবলী / উদ্দেশ্য (Purposes / Objectives of preparing Trial Balance)

-

রেওয়ামিলের উপযোগিতা (Advantages/ usefulness of preparing Trial Balance)

-

রেওয়ামিল প্রস্তুতকরণ কি বাধ্যতা মূলক? (Is preparation of Trial Balance compulsory?)

-

রেওয়ামিলের সীমাবদ্ধতা (Disadvantages/ limitations of preparing Trial Balance):

-

রেওয়ামিল একটি হিসাবখাত নয় (Trial Balance is not at all an Account)

-

কিছু হিসাব সংক্রান্ত ভুলত্রুটি যা রেওয়ামিল প্রস্তুতকালে নির্ধারণ করা সম্ভব (Types of Errors that can be detected while preparing Trial Balance)

-

কিছু হিসাব সংক্রান্ত ভুলত্রুটি যা রেওয়ামিল প্রস্তুতকালে নির্ধারণ করা সম্ভব নয় (Types of Errors that cannot be detected while preparing Trial Balance)

-

Chapter Revision - Trial Balance

-

Practical sums Trial Balance4 Topics

-

Chapter Exercise2 Topics|1 Quiz

-

Chap 8 - Final AccountsVideos - Final Accounts32 Topics

-

Introduction to Final Accounts

-

Trading Account

-

Example 1 on Trading Account 1

-

Example 2 on Trading Account

-

Puzzle Round 1

-

Puzzle Round 2

-

Profit and Loss Account

-

Example on Profit and Loss Account

-

Example on Trading and Profit and Loss Account

-

Operating Profit

-

Example on Operating Profit and Net Profit

-

Balance Sheet and its format

-

Example on Balance Sheet

-

Example 1 of Final Accounts without Adjustments

-

Example 2 of Final Accounts with Adjustments and GST

-

Various Adjustments in Final Accounts Part 1

-

Various Adjustments in Final Accounts Part 2 (Interest on Capital and Interest on Drawings)

-

Various Adjustments in Final Accounts Part 3

-

Various Adjustments in Final Accounts Part 4

-

Various Adjustments in Final Accounts Part 5

-

Various Adjustments in Final Accounts Part 6

-

Various Adjustments in Final Accounts Part 7

-

Adjustment relating to Final Accounts Part 8

-

Sum 1 on Final Accounts

-

Sum 2 on Final Accounts

-

Sum 3 on Final Accounts

-

Sum 4 on Final Accounts

-

Sum 5 on Final Accounts

-

Sum 6 on Final Accounts

-

Sum 7 on Final Accounts

-

Sum 8 on Final Accounts with GST

-

Revision on Final Accounts

-

Introduction to Final Accounts

-

Module 1 - Final Accounts Without Adjustments34 Topics

-

ভূমিকা (Introduction)

-

কেন একটি প্রতিষ্ঠানের ক্ষেত্রে আর্থিক বিবরনী প্রস্তুত করা অত্যন্ত গুরুত্বপূর্ণ? (Why Preparation Financial Statements is so much important for a business concern?)

-

আর্থিক বিবরণীর সীমাবদ্ধতা সমূহ (Limitations or Disadvantages of Financial Statements)

-

আর্থিক বিবরণীর ব্যাবহারকারীগণ কারা? (Who are the users of Financial Statements?)

-

আর্থিক বিবরণী (The Financial Statements)

-

ক্রয়বিক্রয় হিসাব (The Trading Account)

-

ক্রয়বিক্রয় হিসাবের বিষয়সমূহ (Items that are include in Trading Account)

-

ক্রয়বিক্রয় হিসাব প্রস্তুতকরণ (Preparation of Trading Account)

-

ক্রয়বিক্রয় হিসাবের জের নির্ণয় ও মোট মুনাফা অথবা মোট ক্ষতি নির্ধারণকরন (Balancing Mechanism of Trading Account and Determination of Gross Profit or Gross Loss)

-

লাভ ক্ষতি হিসাব (The Profit & Loss Account)

-

লাভ ক্ষতি হিসাবের বিষয়সমূহ (Items that are included in Profit & Loss Account)

-

লাভক্ষতি হিসাবের জের নির্ণয় ও নীট মুনাফা অথবা নীট ক্ষতি নির্ধারণকরন (Balancing Mechanism of Profit & Loss Account and Determination of Net Profit or Net Loss)

-

লাভক্ষতি হিসাব প্রস্তুতকরণ (Preparation of Profit & Loss Account)

-

কার্যকরী মুনাফা (Operating Profit)

-

কার্যকরী মুনাফা এবং নীট মুনাফার মধ্যে সম্পর্ক (Relation between Operating Profit and Net Profit)

-

মোট মুনাফা এবং নীট মুনাফার পার্থক্য (Difference between Operating Profit and Net Profit)

-

ক্রয়বিক্রয় হিসাব এবং লাভক্ষতি হিসাবের মধ্যে পার্থক্য (Difference between Trading Account and Profit & Loss Account)

-

উদ্বর্তপত্র (Balance Sheet)

-

উদ্বর্তপত্র সম্পর্কিত বিষয়সমূহ (Items related to the Balance Sheet)

-

সম্পত্তি এবং দায়ের মধ্যে পার্থক্য (Difference between Assets and Liabilities)

-

স্থায়ী সম্পত্তি এবং চলতি সম্পতির মধ্যে পার্থক্য (Difference between Assets and Liabilities)

-

উদ্বর্তপত্রের সম্পত্তি ও দায়সমূহের বিন্যাসকরণ ও তার ধারণা (Marshalling of Assets & Liabilities in Balance sheet and the Concept of a Marshalling.)

-

উদ্বর্তপত্র প্রস্তুতকরণ (Preparation of a Balance Sheet.)

-

উদ্বর্তপত্র কি একটি হিসাবখাত? (Is Balance Sheet an Account?)

-

উদ্বর্তপত্র কি শুধু একটি জেরের বিবরণীমাত্র? অথবা উদ্বর্তপত্রকে একটি উদবৃত্তের তালিকা বললে কি ভুল হবে? (Is Balance Sheet only a Statement of Balances? or would it be wrong to name Balance Sheet as a List of Balances?)

-

উদ্বর্তপত্র কি শুধুমাত্র একটি সম্পত্তি ও দায়ের বিবরণী? (Is Balance Sheet a statement of Assets and Liabilities?)

-

উদ্বর্তপত্র প্রস্তুতকরণ কি একটি প্রতিষ্ঠানের ক্ষেত্রে বাধ্যতামূলক? (Is preparation of Balance Sheet mandatory in case of an organization?)

-

রেওয়ামিল এবং উদ্বর্তপত্রের মধ্যে পার্থক্য (Difference between Trial Balance and Balance Sheet)

-

উদ্বর্তপত্র একটি দ্বিতীয় রেওয়ামিল’- ব্যাখ্যা কর। (State that: ‘Balance Sheet is Second Trial Balance’)

-

উদ্বর্তপত্র কি প্রতিষ্ঠানের সঠিক আর্থিক অবস্থার প্রতিফলক হিসাবে কাজ করে? (Does the Balance Sheet reflect the True Financial Position of a Concern?) অথবা, উদ্বর্তপত্রের সীমাবদ্ধতা (Limitation of Balance Sheet)

-

লাভক্ষতি হিসাব এবং উদ্বর্তপত্রের মধ্যে পার্থক্য (Difference between Profit & Loss Account and Balance Sheet)

-

লাভক্ষতি হিসাব এবং উদ্বর্তপত্রের মধ্যে সম্পর্ক (Relation between Profit & Loss Account and Balance Sheet)

-

চূড়ান্ত হিসাবখাত (Final Accounts)

-

Chapter Revision - Module 1 - Final Accounts Without Adjustments

-

ভূমিকা (Introduction)

-

Module 2 - Final Accounts with Adjustments5 Topics

-

সূচনা (Introduction)

-

চূড়ান্ত হিসাবে মিলকরণের পূর্বে মিলকরণ সম্বন্ধীয় কিছু প্রাথমিক ধারণা (Some fundamentals ideas of Adjustments and their role in Financial Statement)

-

চূড়ান্ত হিসাবের সঙ্গে সংস্রবিত কিছু গুরুত্বপূর্ণ মিলকরণ (Some important adjustment, which may require at time of preparation of Financial Statement)

-

আরও কতিপয় জ্ঞাতব্য সমন্বয় সংক্রান্ত বিষয় (Some more items regarding Adjustments -students should know)

-

Chapter Revision - Module 2 - Final Accounts with Adjustments

-

সূচনা (Introduction)

-

Module 2 - Chapter Exercise1 Topic|1 Quiz

-

Module 3 - Accounting Equation8 Topics

-

ভূমিকা (Introduction)

-

হিসাবনিকাশ সমীকরনের অর্থ (Meaning of Accounting Equation)

-

হিসাব-নিকাশ সমীকরণের বিন্যাস (Arranging order of Accounting Equation)

-

হিসাবনিকাশ সমীকরণের গুরুত্ব (Importance of accounting equation)

-

হিসাবনিকাশ সমীকরণ সংক্রান্ত হিসাবনিকাশের মূল নীতি (Fundamental Accounting Principal of Accounting Equation)

-

ব্যাখ্যা

-

আরও কিছু নানাবিধ লেনদেন (Treatment of Miscellaneous transactions in accounting equation)

-

Chapter Revision - Module 3 - Accounting Equation

-

ভূমিকা (Introduction)

-

Module 3 - Chapter Exercise2 Topics|1 Quiz

-

Chap 9 - NPOVideos - NPO25 Topics

-

Basic concepts of NPO

-

Introduction and Format of Receipts and Payments Account

-

Example on Receipts and Payments Account

-

Concept of Income and Expenditure and Example

-

Format of Income and Expenditure Account

-

Sum on Income and Expenditure Account

-

Case 1 - Subscription amount

-

Case 2 - Subscription amount

-

Case 3 - Subscription amount

-

Case 4 - Subscription amount

-

Example 1 on Income and Expenditure Account

-

Example 2 on Income and Expenditure Account

-

Example 3 on Income and Expenditure Account

-

Example 4 on Income and Expenditure Account

-

Format of Balance Sheet for NPO

-

Example 1 on Income and Expenditure Account and Balance Sheet

-

Example 2 on Income and Expenditure Account and Balance Sheet

-

Example 3 on Income and Expenditure Account and Balance Sheet

-

Example 4 on Income and Expenditure Account and Balance Sheet

-

Various cases on Special Fund

-

Preparation of Income and Expenditure Account and Balance Sheet on Special Fund Case

-

Example 1 Preparation of Receipts and Payments Account from Income and Expenditure Account

-

Example 2 Preparation of Receipts and Payments Account from Income and Expenditure Account

-

Preparation of Balance Sheet from Receipts and Payments Account and Income and Expenditure Account

-

Recap Session on NPO

-

Basic concepts of NPO

-

NPO - ইউনিট – ১12 Topics

-

ভূমিকা (Introduction)

-

অ-মুনাফা সন্ধানী / অ-মুনাফাভোগী প্রতিষ্ঠানের সংজ্ঞা (Definition of Non-Profit Seeking Organisaion)

-

অমুনাফা সন্ধানী প্রতিষ্ঠানের বৈশিষ্ট্য (Features and Characteristics of Non-profit Organization)

-

মুনাফা সন্ধানী প্রতিষ্ঠান এবং অ-মুনাফা সন্ধানী প্রতিষ্ঠানের পার্থক্য (Profit seeking organisation V/s Non-profit seeking Organisation)

-

অ-মুনাফা সন্ধানী প্রতিষ্ঠানের হিসাবনিকাশকরণ (Accounting for Non-profit seeking Organization)

-

প্রাপ্তি এবং আয়ের মধ্যে পার্থক্য (Difference between Receipts and Income)

-

প্রদান এবং ব্যয়ের মধ্যে পার্থক্য (Difference between Payments and Expenditure)

-

একটি অমুনাফাভোগী প্রতিষ্ঠানের উদ্বর্ত পত্র (The Balance Sheet of a Non-profit Seeking Organization [NPO])

-

কতিপয় গুরুত্বপূর্ণ আয় এবং ব্যয় সংক্রান্ত বিষয় যেগুলির ক্ষেত্রে সমন্বয়ের প্রয়োজনীয়তা দেখা যায় যখন একটি প্রদত্ত প্রাপ্তি প্রদান হিসাব থেকে আয়-ব্যয়ের হিসাব প্রস্তুত করা হয়

-

একনজরে সমন্বয় সাধনের মারফৎ প্রাপ্তি-প্রদান হিসাব থেকে আয়-ব্যয়ের হিসাব এবং অন্তিম উদ্বর্ত পত্র প্রস্তুত প্রণালী (Preparation of Income and Expenditure Account and Balance Sheet from the given Receipts & Payment Account)

-

এক নজরে আয়-ব্যয় হিসাব সংক্রান্ত কিছু সমন্বয় ও উদ্বর্ত পত্রে তার অবস্থান (Some of Adjustments Relating to Income and Expenditure A/c and effect in balance Sheet thereon, at a glance)

-

Chapter Revision - NPO - ইউনিট – ১

-

ভূমিকা (Introduction)

-

NPO - ইউনিট – ২4 Topics

-

ভূমিকা (Introduction)

-

আয়-ব্যয় হিসাব থেকে প্রাপ্তি-প্রদান হিসাব প্রস্তুতকরণ (Preparation of Receipts & Payments Account from a given Income & Expenditure Account)

-

প্রাপ্তি ও প্রদান হিসাব এবং আয় ও ব্যয়ের হিসাবের মধ্যে পার্থক্য (Receipts & Payments Account v/s Income & Expenditure Account)

-

Chapter Revision - NPO - ইউনিট – ২

-

ভূমিকা (Introduction)

-

Chapter Exercise2 Topics|1 Quiz

-

Chap 10 - Single EntryVideos - Single Entry13 Topics

-

Introduction to Single Entry

-

Format of Single Entry

-

Example 1 on Single Entry

-

Example 2 on Single Entry

-

Example 3 on Single Entry

-

Example 4 on Single Entry

-

Example 5 on Single Entry

-

Example 6 on Single Entry

-

Example 7 Single Entry First Method based on Partnership

-

Conversion Method Example 1

-

Conversion Method Example 2 and 3

-

Conversion Method Example 4

-

Recap Session on Single Entry System

-

Introduction to Single Entry

-

ভুমিকা (Introduction)

-

অসম্পূর্ণ তথ্য ভিত্তিক হিসাবনিকাশ করণ পদ্ধতির ব্যবহারিক ক্ষেত্র (Who are the users of Single-Entry System – Practical Implementations)

-

একতরফা দাখিলা পদ্ধতির সংজ্ঞা (Definition of Single-Entry System)

-

একতরফা দাখিলা পদ্ধতির বৈশিষ্ট্য (Salient features of Single-Entry System)

-

একতরফা দাখিলা পদ্ধতির উপযোগিতা (Utility / Advantages of Single-Entry System)

-

একতরফা দাখিলা পদ্ধতির সীমাবদ্ধতা (Limitations / Disadvantages of Single-Entry System)

-

দ্বিতরফা দাখিলা পদ্ধতি বনাম একতরফা দাখিলা পদ্ধতি (Double Entry System v/s Single Entry System)

-

একতরফা দাখিলা পদ্ধতিতে হিসাবনিকাশকরণ (Accounting for an Incomplete Record or Single Entry)

-

বৈষয়িক বিবরণীর সঙ্গে উদ্বর্ত পত্রের পার্থক্য (Difference between Statement of Affairs & Balance Sheet)

-

Chapter Revision - Single Entry

-

Chapter Exercise2 Topics|1 Quiz

-

Chap 11 - Bill of ExchangeVideos - Bill of Exchange14 Topics

-

Introduction to Bill

-

4 Cases on how the Seller can use the Bill

-

Date of Maturity

-

Examples on Date of Maturity Calculation

-

Theory on Bills of Exchange

-

Example 1 Based on Honour of Bill

-

Example 2 Based on Honour of Bill

-

Example 3 Based on Honour of Bill

-

Example 4 Based on Honour of Bill

-

Example 5 Based on Honour of Bill

-

Comprehensive Example 6 Based on Honour of Bill

-

Concept of Dishonour of Bill

-

Example 2 Dishonour of Bill

-

Example 3 Dishonour of Bill

-

Introduction to Bill

-

ইউনিট – ১ - Bill of Exchange4 Topics

-

ইউনিট – ২ - Bill of Exchange18 Topics

-

ভূমিকা (Introduction)

-

বানিজ্যিক হুন্ডির সঙ্গে সংস্রবিত কিছু গুরুত্বপূর্ণ এবং তাৎপর্যপূর্ণ শব্দগুচ্ছ – তার ব্যবহার ও প্রয়োগ (Some of the Important Terms Associated with Bills of exchanges – Uses and Implementations)

-

বানিজ্যিক হুন্ডি ও প্রত্যর্থপত্র হিসাবনিকাশকরণের ক্ষেত্রে ব্যবহৃত দাখিলা সমূহ ও তার ব্যাখ্যা (Entries required for Bills of Exchange & Promissory Note along with Interpretations)

-

হুন্ডি পরিসমাপ্তির বিভিন্ন উপায় (Different ways of termination of Bill)

-

বাণিজ্যিক হুন্ডির পরিসমাপ্তি ক্ষেত্র – ১

-

বাণিজ্যিক হুন্ডির পরিসমাপ্তি ক্ষেত্র – ২

-

বাণিজ্যিক হুন্ডির পরিসমাপ্তি ক্ষেত্র – ৩

-

বাণিজ্যিক হুন্ডির পরিসমাপ্তি ক্ষেত্র – ৪

-

Illustration 6

-

Illustration 7

-

Illustration 8

-

Illustration 9

-

Illustration 10

-

Illustration 11

-

Illustration 12

-

Illustration 13

-

Illustration 14

-

Chapter Revision - ইউনিট – ২ - Bill of Exchange

-

ভূমিকা (Introduction)

-

Chapter Exercise2 Topics|1 Quiz

-

Chap 12 - Reserves and Surplusভূমিকা (Introduction)

-

সঞ্চিতি (Reserves)

-

সঞ্চিতির শ্রেনীবিভাগ ও সৃষ্টির কারণ (Classification of Reserve and causes of creation)

-

সঞ্চিতি তহবিল (Reserve Fund)

-

সঞ্চিতি তহবিলের সুবিধা (Advantages of Reserve Fund)

-

সঞ্চিতি বনাম সঞ্চিতি তহবিল (Reserve v/s Reserve Fund)

-

সঞ্চিতির হিসাবনিকাশকরণ (Accounting Treatment of Reserves)

-

সঞ্চিতি তহবিলের হিসাবনিকাশকরণ (Accounting Treatment of Reserves Fund)

-

ভবিষ্যৎ ব্যবস্থা / সংস্থান (Provision)

-

ভবিষ্যৎ ব্যবস্থা সৃষ্টির কারণ (Causes of creation of Provision)

-

ভবিষ্যৎ ব্যবস্থার বৈশিষ্ট্য (Features of Provision)

-

ভবিষ্যৎ ব্যবস্থার শ্রেণীবিভাগ (Classification of Provision)

-

সঞ্চিতি বনাম ভবিষ্যৎ ব্যবস্থা (Reserves v/s Provision)

-

পাওনা ঋণ, পাওনা ঋণের প্রকারভেদ, অনিশ্চিত ঋণ এবং অনিশ্চিত ঋণের জন্য ভবিষ্যৎ ব্যবস্থা (Debts Receivable, Classification of Debts Receivable, Doubtful debts & Provision for Doubtful debts)

-

কু-ঋণ এবং ভবিষ্যৎ ব্যবস্থার হিসাবনিকাশকরণ পদ্ধতি (Accounting for Bad Debt and Provision for Bad debt)

-

দেনাদারদের প্রদত্ত বাট্টার জন্য ভবিষ্যৎ ব্যবস্থা এবং তার হিসাবনিকাশকরণ (Provision for Discount on Debtors and its Accounting Treatment)

-

কু-ঋণ পুনরুদ্ধার এবং তার হিসাবনিকাশকরণ (Recovery of Bad Debt and its Accounting Treatment)

-

পাওনাদারদের কাছ থেকে প্রাপ্য বাট্টার জন্য সংরক্ষণ এবং তার হিসাবনিকাশকরণ (Provisions / Reserves for Discount on Creditors and its Accounting Treatments)

-

Chapter Revision - Reserves and Surplus

-

Chapter Exercise2 Topics

-

Chap 13 - DepreciationVideos - Depreciation and Bad Debts20 Topics

-

Bad Debt Theory

-

Example 1 Bad Debt

-

Example 2 Bad Debt

-

Provision for Discount on Creditors

-

Introduction to Depreciation

-

Methods of Depreciation

-

Straight Line Method vs Written Down Value Method

-

Example 1 on Straight Line Method

-

Example 2 on Straight Line Method

-

Example 3 on Straight Line Method

-

Example 4 on Straight Line Method

-

Example 5 on Straight Line Method

-

Example 1 on WDV Method

-

Example 2 on WDV Method

-

Example 3 on WDV Method

-

Example 4 on WDV Method

-

Example 5 on WDV Method

-

Introduction to Provision for Depreciation

-

Example 1 on Provision for Depreciation

-

Example 2 on Provision for Depreciation

-

Bad Debt Theory

-

ভুমিকা (Introduction)

-

অবচয়ের সংজ্ঞা (Definition of Depreciation)

-

অবচয়ের কারণ সমূহ (Causes of Depreciation)

-

অবচয়ের বৈশিষ্ট্য (Features of Depreciation)

-

অবচয়ের ধার্য করার কারণ সমূহ (Needs or Causes of Charging Depreciation)

-

অবচয়ের সঙ্গে সংস্রবিত কিছু গুরুত্বপূর্ণ শব্দগুচ্ছ (Some important terms associated with calculation of depreciation)

-

অবচয় নির্ধারণের বিভিন্ন কৌশল (Methods of charging depreciation)

-

অবচয় এবং অবচয়ের জন্য ভবিষ্যৎ ব্যবস্থার মধ্যে পার্থক্য (Difference between Depreciation and Provision for Depreciation)

-

অবচয় ধার্য করার বিভিন্ন পদ্ধতি (Various methods for calculating Depreciation)

-

স্থির কিস্তি বা সরলরৈখিক পদ্ধতি (Fixed Installment or Straight-Line Method): (Where Depreciation is charged and absorbed to concerned asset account without opening Provision for Depreciation Account)

-

ক্রমহ্রাসমান তহবিল বা ক্রমহ্রাসমান জের পদ্ধতি (Reducing Balance or Diminishing Balance Method): (Where Depreciation is charged and absorbed to concerned asset account without opening Provision for Depreciation Account)

-

স্থির কিস্তি পদ্ধতি এবং ক্রমহ্রাসমান জের পদ্ধতির মধ্যে পার্থক্য (Distinguish Between Fixed Installment Method and Reducing Balance Method)

-

অবচয় কি একটি ফান্ডের উৎস? (Is Depreciation a Source of Fund?)

-

সম্পত্তি ক্রয় এবং বিক্রয় (Purchase of asset and Sale or disposal of asset)

-

কারবারে সম্পত্তির অবচয় ধার্য করার কার্যকরী দিন (Effective usage of Assets into the Business)

-

সম্পত্তি বিক্রয় জনিত লাভ বা ক্ষতি (Profit or Loss on Sale of Fixed Asset)

-

স্থির কিস্তি পদ্ধতির কিছু ব্যবহারিক উদাহরণ (Illustrative examples based on charging Depreciation under Straight Line Method or Fixed Installment Method)

-

ক্রমহ্রাসমান জের পদ্ধতির কিছু ব্যবহারিক উদাহরণ (Illustrative examples based on charging Depreciation under Diminishing Balance Method or Written Down Value Method)

-

কিছু ব্যবহারিক উদাহরণ যেক্ষেত্রে অবচয়ের জন্য ভবিষ্যৎ ব্যবস্থা পদ্ধতি গ্রহণ করা হয়েছে (Illustrative Examples where Provision for Depreciation or Accumulated depreciation Account is opened)

-

Chapter Revision - Depreciation

-

Chapter Exercise2 Topics|1 Quiz

-

Practical sums Final Accounts3 Topics

-

JOURNAL UNDER GST9 Topics

-

পণ্য ও পরিষেবা কর কি? (What is GST?)

-

Output GST (CGST, SGST বা IGST) এবং Input GST (CGST, SGST IGST) -এর মধ্যে ভারসাম্য বা সমন্বয় সাধন (Set-off between Input and Output GST or Input tax credit Set-off):

-

GST-এর বিপরীত ক্রম (Reversal of GST):

-

GST সংক্রান্ত বিভিন্ন দাখিলা সম্পর্কে পরিচিতি ও তার প্রয়োগ (Accounting entries relating to GST and its implementations):

-

Output GST সংক্রান্ত লেনদেন সমূহ (Transactions relating to Output GST):

-

Input এবং Output GST প্রয়গের ক্ষেত্র সমূহ

-

GST বিপরীত ক্রম সংক্রান্ত লেনদেন সমূহ (Transactions relating to Reversal of GST):

-

Revesal of GST প্রয়োগের ক্ষেত্র সমূহ

-

এখন একনজরে দেখে নেওয়া যাক GST সম্বলিত কিছু লেনদেনের জাবেদাকরণঃ Transactions and Journal entries on which GST is to be paid or payable i.e., Input GST (CGST, SGST, IGST):

-

পণ্য ও পরিষেবা কর কি? (What is GST?)

-

Practical sums Single Entry5 Topics

-

Practical sums Bill of Exchange6 Topics

-

Practical sums Depreciation2 Topics

-

Practical sums Ledger4 Topics

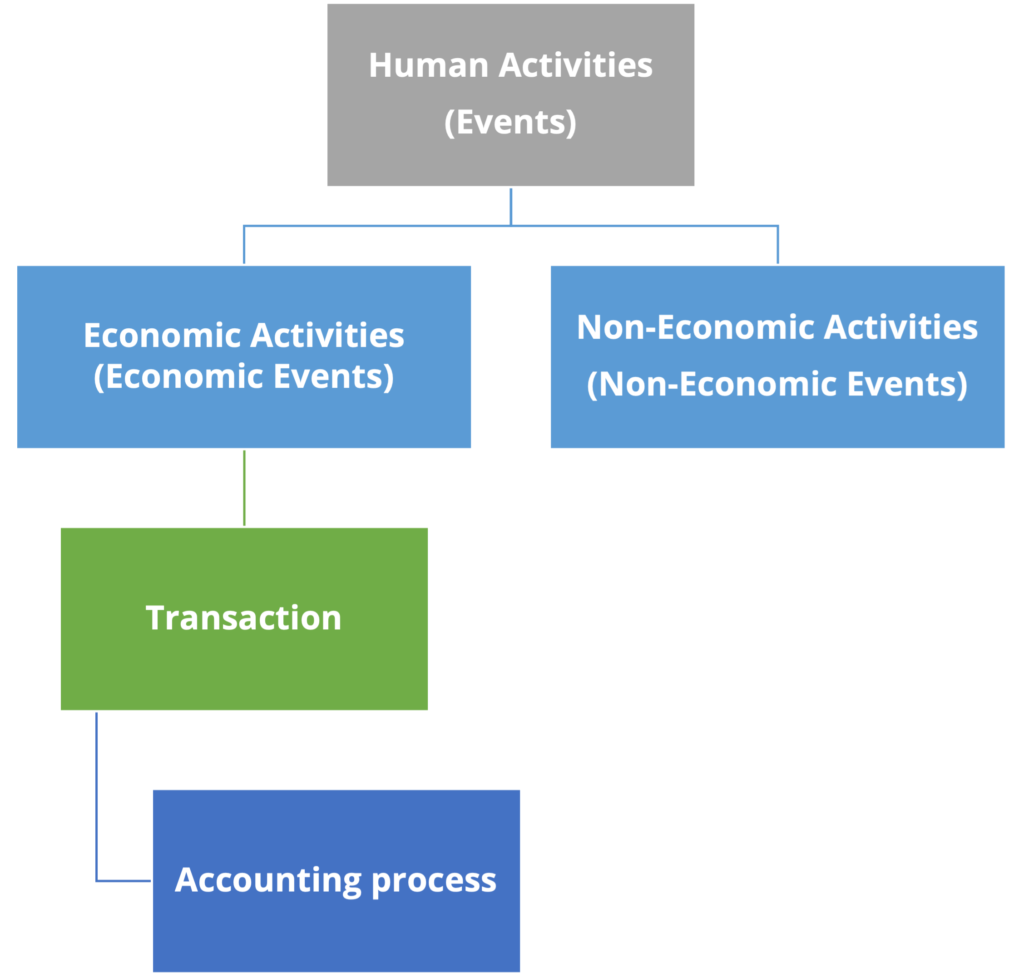

ভূমিকা (Introduction to Events and Transactions)

Since primitive times, (human) beings were engaged in some kind of activity to carry out and maintain their livelihood. Without the help of such (human) activities, a society cannot be developed and enriched. To fulfil their needs, satisfaction and desires humans engaged themselves in doing some kind of activities according to their different skills.

Human life is built around various kinds of activities to be performed. Every human being engages themselves in some or the other activity throughout the day. For e.g., brushing, studying, reading newspapers, house chores done by housewives, working at offices, etc. Such activities are termed as Human activities.

Some of these human activities are undertaken for direct economic benefits like, monetary gains; and some other such activities do not have any economic benefits i.e. done for personal satisfaction like, charity, helping the needy, etc.

Classification of human activities:

Human activities may be categorised into two namely,

- Economic activity

- Non-economic activity

Non-economic activities are mainly performed to mainly honour and fulfil our social, cultural, patriotic, emotional and religious obligations. Non-economic activities are inspired by sentiments and emotions such as love for the family, desire to help the poor and needy and show love and respect for the country where a person is living. Such Non-economic activities are not concerned with any of the monetary gains but getting personal-level satisfaction and happiness is the true test of such activities.

Whereas, Economic activities are under taken with the object of earning money and acquisition of wealth to secure an individual from future uncertainties.

Our entire concept of accounting is concerned with the economic activities having some characteristics. Mainly it consists of economic motives like, earning money and acquiring wealth and finally bring down an economic gain and economic growth.

Every economic activity must be productive i.e., it involves production, distribution an exchange of goods and services for satisfying human needs and wants which ultimately creates wealth for the society. Every economic activity comprises of the four important elements – land, labour, capital and entrepreneur. These elements are termed as – “Factors of Production”. Efficient planning of these factors of production along with proper allocation of scare resources helps to obtain maximum output.

It should even be noted that economic activities should be legally valid i.e., it should be lawful and should be ensured that such activities must not disturb the society as a whole and must not be opposed to the public interest and must be maintained in accordance with the expectations and norms of the society.

In other words, every businessman or business-house works hard to earn profits from their economic activities, which they have offered to the society. If the economic activities offer clear results about the economic rewards to a businessman, it stimulates them to invest more amount to reap that profit by bearing the risk of uncertainties.

Every trader / businessman can be sure of the results of their business activities as they know the work undertaken by them for their concern. As the economic activities in a business are huge in number, complicated and also at times requires documentary evidences to be maintained, it is quite difficult for the trader/ businessman to remember all such activities. It thus requires a systematic and scientific record-keeping of such business activities. In other words, it requires proper accounting procedure of such business activities.

সৃষ্টির ঊষালগ্নে সভ্যতার জন্ম। সভ্যতার ইতিহাস ও বিবর্তন পর্যালোচনা করলে দেখা যায় যে এক মাত্র মনুষ্য সম্পদই অগ্রগতির ধারাবাহিকতাকে বজায় রেখেছে এবং এগিয়ে নিয়ে গেছে। এই ধারাবাহিকতা কে বজায় রাখার জন্য তাকে বারংবার প্রবৃত্ত হতে হয়েছে বিভিন্ন ধরণের কার্যাবলীতে। মনুষ্য কার্যাবলীর দ্বারাই সৃষ্টি হয়েছে সমাজের। ক্রমে ক্রমে সভ্যতার অগ্রগতির সঙ্গে সঙ্গে মনুষ্য সমাজ তথা মানুষের চাহিদার সৃষ্টি হয়েছে। সৃষ্টির প্রাথমিক পর্যায় মানুষ তার প্রয়োজনীয় চাহিদা স্বয়ং সম্পূর্ণ ভাবে পূরণ করতে সমর্থ হলেও পরবর্তী পর্যায় চাহিদার বিচিত্র এবং মাত্রাধিক্য ঘটার কারণে তার একার পক্ষে তার প্রয়োজনীয় সকল চাহিদা পূরণ করা আর সম্ভবপর হল না, উদ্ভব হল এমন এক সমাজ যেখানে সমাজবদ্ধ সকলে তার নিজ নিজ দক্ষতা অনুযায়ী বিভিন্ন কর্মকে বেছে নিয়ে সামগ্রিক ভাবে সামাজিক চাহিদা পূরণে উদ্যত হলেন।

সুতরাং বলা যায় মনুষ্য কার্যাবলী মনুষ্য সমাজের ধারক ও বাহক। এই মনুষ্য কার্যাবলী গুলিকে বিশেষণ করলে আমরা মূলত দুই ধরণের কার্যাবলী খুঁজে পাই। একটি হল অ-অর্থনৈতিক মনুষ্য কার্যাবলী (Non-Economic Human Activities) এবং অপরটি হল অর্থনৈতিক মনুষ্য কার্যাবলী (Economic Human Activities

অ-অর্থনৈতিক কার্যাবলী গুলি মূলত সামাজিক (Social), সাংস্কৃতিক (Cultural), দেশাত্মক (Patriotic), ধার্মিক (Religious) ইত্যাদি বিষয় গুলিকে ধারণ করে এবং বহন করে নিয়ে চলে। এই কার্যাবলীর সঙ্গে অর্থনৈতিক কার্যাবলীর সরাসরি কোনো যোগাযোগ নেই। অপরদিকে অর্থনৈতিক কার্যাবলী গুলি মূলত আয়ের সঙ্গে সরাসরি সম্পর্ক যুক্ত। যে আয় বর্তমান এবং ভবিষ্যৎ চাহিদা পূরণ এবং ভবিষ্যৎ সম্পর্ক বৃদ্ধিতে প্রত্যক্ষ ভূমিকা পালন করে।

আমরা আমাদের দৈনন্দিন নিত্যনৈমিত্তিক জীবনেও একই সঙ্গে পাশাপাশি অর্থনৈতিক এবং অ-অর্থনৈতিক কার্যাবলীর সমাহার লক্ষ করে থাকি। যেমন একটি পরিবারে সকাল বেলা শিশুরা বিদ্যা আহরণের জন্য বিদ্যালয় যায়, যে অর্জিত বিদ্যা তাকে ভবিষ্যৎ বিভিন্ন অর্থনৈতিক কাজে প্রবৃত্ত হতে সাহায্য করে। বাড়িতে যে বা যারা মূল আয়ের কেন্দ্র তারা তাদের কর্মস্থলে যাত্রা করেন আয় লাভের আশায়, যা একটি অর্থনৈতিক কার্যাবলী হিসেবে চিহ্নিত। দিনান্তে বাড়ির সকল সদস্য নিজ নিজ কর্মস্থল থেকে নিজ নিজ গৃহে প্রত্যাবর্তন করেন। শিশুরা পুণরায় পাঠ্যে মনোনিবেশ করে অতঃপর কিছু বিনোদন সম্পন্ন করে নৈশভোজ সম্পন্ন করে একটি দিনের পরিসমাপ্তি ঘটে। অ-অর্থনৈতিক কার্যাবলী গুলির মধ্যে পিতা ও মাতার সন্তানের প্রতি স্নেহ ও ভালবাসা, সন্তানের পিতা মাতা ও অন্যান্য গুরুজনদের প্রতি শ্রদ্ধা ও ভালবাসা, প্রতিটি নাগরিকের নিজ দেশের প্রতি অকৃত্রিম ভালোবাসা, কোনো দুস্থ মানুষকে সাহায্য করা ইত্যদি বিষয় গুলি অন্তর্ভুক্ত।

ওপরের উদাহরণটি পর্যালোচনা করলে বোঝা যায় যে মনুষ্য জীবন বেশ কিছু অর্থনৈতিক ও অ-অর্থনৈতিক কার্যাবলীর ফলে সৃষ্ট ধারবাহিক এক কার্যক্রম। অ-অর্থনৈতিক কার্যাবলী গুলির সঙ্গে অর্থের কোনো সম্পর্ক নেই কিন্তু স্বছন্দ জীবনযাপনের জন্য এবং মানসিক প্রশান্তি ও সুখ-শান্তি অর্জন প্রভৃতি অ-অর্থনৈতিক কার্যাবলীর ধারাবাহিকতা কে বজায় রাখার জন্য অর্থনৈতিক কার্যাবলী গুলি অত্যাবশ্যক।

পরিশেষে বলা যায় মনুষ্য সমাজ কিছু ধারাবাহিক বা বিচ্ছিন্ন অর্থনৈতিক এবং অ-অর্থনৈতিক ঘটনার সমাহার।

আমাদের হিসাব সংক্রান্ত সমগ্র আলোচনা অর্থনৈতিক ঘটনা বা কার্যাবলীর সংমিশ্রণে গঠিত। একটি অর্থনৈতিক কার্যাবলী সংক্রান্ত ঘটনা মূলত পরিচালিত হয় অর্থ উপার্জন, সম্পদ আহোরণ এবং পরিশেষে অর্থনৈতিক উন্নতি এবং সামগ্রিক জীবনযাত্রার মানোন্নয়নের মাধ্যমে। যেকোনো অথনৈতিক কার্যাবলীর সঙ্গে উৎপাদন (Production), দ্রব্য বা সেবার বিনিময় ও বণ্টন (Exchange and Distribution of Goods and Services) এবং যার মারফৎ মনুষ্য চাহিদা পূরণ ও পরিশেষে সম্পদ আহরনের মাধ্যমে সামাজিক উন্নতি প্রতিফলিত হয়।

অথনৈতিক কার্যাবলীর মূল উপাদান হল জমি (Land), শ্রম (Labour), মূলধন (Capital) এবং উদ্যোগ (Entrepreneurship)। এই উপাদান গুলিকে একত্রে উৎপাদনের উপাদান হিসেবে পরিচিত যার মারফৎ প্রকৃতি দত্ত সম্পদের আহরণ, প্রকৃত ব্যবহার এবং তার বণ্টন সম্ভব হয়।

প্রসঙ্গত উল্লেখযোগ্য কারবার, কারবারির কারবার সংক্রান্ত ঝুঁকি গ্রহণের পুরষ্কার স্বরূপ মুনাফা প্রদান করে, একাধিক কর্ম সংস্থানের সুযোগ করে, দ্রব্য বা সেবার উৎপাদন বা বিনিময় মারফৎ মনুষ্য চাহিদা পূরণ করে, সামাজিক উন্নয়নের ধারাকে অব্যহত রাখে এবং জাতীয় সম্পদ বৃদ্ধিতে বিশেষ অবদান সৃষ্টি করে। কাজেই বলা যায় কারবার সংক্রান্ত সকল কার্যাবলী বা ঘটনা চূড়ান্ত ভাবে অর্থনৈতিক কার্যাবলী। আগেই উল্লেখ করা হয়েছে মুনাফা হল একজন কারবারির কারবার সক্রান্ত ঝুঁকি বহনের পুরষ্কার যা তাকে অন্যান্য ঝুঁকি মূলক বিনিয়গে উৎসাহিত করে তলে এবং তিনি নতুন নতুন উদ্যোগ গ্রহণ করেন যার সু-ফল সামগ্রিক ভাবে একটি সমাজ গ্রহণ করে এবং বহু ক্ষেত্রে এই সুফলের প্রভাব কারবারির নিজের দেশের সীমানা পেরিয়ে বহিঃদেশেও প্রতিফলিত হয়।

একজন কারবারি একটি অর্থনৈতিক কার্যাবলীর একজন মূল কাণ্ডারি হিসেবে চিহ্নিত। তার দায়বদ্ধতাও প্রচুর। তিনি এমন কোনো উদ্যোগ গ্রহণ করে তাতে অর্থ নিবেশ করবেন না যাতে সমাজ বিশেষভাবে ক্ষতিগ্রস্ত হয় এবং একমাত্র মুনাফা অর্জনই একজন সৎ কারবারির উদ্দেশ্য হওয়া মোটেই উচিত নয়। বরং ন্যায্য মূল্যের বিনিময় উৎপাদিত পণ্য বা সেবার সরবরাহ করে জনজীবনের উন্নতি সাধনের মাধ্যমে সামাজিক উন্নতিবিধান তার অন্যতম উদ্দেশ্য হওয়া উচিত।

প্রতিটি কারবারি প্রতিষ্ঠান এবং তার প্রতিষ্ঠাতা দিনান্তে কারবার মারফৎ তার উপার্জন কি হল সেই তথ্যটি জানার জন্য বিশেষ ভাবে উৎসাহী থাকেন এবং একটি ধারাবাহিক প্রতিষ্ঠানে প্রতিনিয়ত অজস্র অর্থনৈতিক ঘটনা যেমন দ্রব্য ক্রয় বিক্রয়, কর্মীদের বেতন প্রদান, কারবারের বৈদ্যুতিক খরচ, কারবার পরিচালন সংক্রান্ত খরচ প্রভৃতি নানাবিধ খরচের সম্মুখিন হতে হয় এবং কারবারের কলেবর বৃদ্ধির সঙ্গে সঙ্গে এই অর্থনিতক ঘটনা গুলির সংখ্যাধিক্যও ঘটতে থাকে। তখন আর কারবারির পক্ষে বিপুল সংখ্যক এবং বৈচিত্র্যপূর্ণ অর্থনৈতিক ঘটনা সমাহার নিজ মস্তিস্কে ধারন করা সম্ভবপর হয় না। তিনি তখন সম্পাদিত অর্থনৈতিক ঘটনা গুলির পর্যায়ক্রমে লিপিবদ্ধ করেনে উদ্যত হন এবং যা অতীতে সম্পাদিত অর্থনৈতিক ঘটনা গুলির ভবিষ্যৎ প্রামাণ্য দলিল হিসাবে কার্যকরী ভূমিকা পালন করে।

আমাদের পরবর্তী আলোচনা সমগ্রই দারিয়ে রয়েছে একটি কারবারে পর্যায়ক্রমে ঘটে যাওয়া অর্থনৈতিক ঘটনা গুলির বিজ্ঞান সম্মত লিপিবদ্ধ করণ প্রণালী এবং তার বিশ্লেষণ পরিশেষে এই সকল অর্থনৈতিক ঘটনা গুলি সংঘটনের ফলে একজন কারবারি তার কারবার সংক্রান্ত ঝুঁকি গ্রহণ কালে ঠিক কত পরিমাণ মুনাফা অর্জন করতে সমর্থ হলেন যা তিনি ঝুঁকি বহন করার পুরষ্কার বাবদ পেলেন এবং কাম্য মুনাফা তাকে আরও ঝুঁকি বহন করে কারবার স্থাপনের জন্য অনুপ্রেরণা যোগাবে।

উপরোক্ত বিষয়টি কে নিম্নলিখিত ছকের মাধ্যমে বোঝানো যেতে পারে

To distinguish human activity from the economic activity let us become familiar with the term “Event” and the term “Transaction” and try to differentiate the term transaction from the term event.